Property insurance in Spain explained for foreign buyers

TL;DR:

- Property insurance in Spain covers the home’s structure, contents, and liability within a single policy.

- Buyers should declare whether a property is a holiday or permanent residence to ensure adequate theft cover during vacancy periods.

Property insurance in Spain, known as seguro de hogar, covers the structure of your home, its contents, and your liability to third parties, all within a single annual policy. For international buyers purchasing in areas such as Marbella, Mallorca, Ibiza, Málaga, and Barcelona, understanding how this cover works is one of the most practical steps you can take before completing a purchase. The Spanish insurance market is generally more affordable than in the UK or Northern Europe, and natural disaster cover is built in via the Consorcio de Compensación de Seguros. This guide covers what is property insurance Spain explained in plain terms, so you can protect your investment with confidence.

What does property insurance in Spain actually cover?

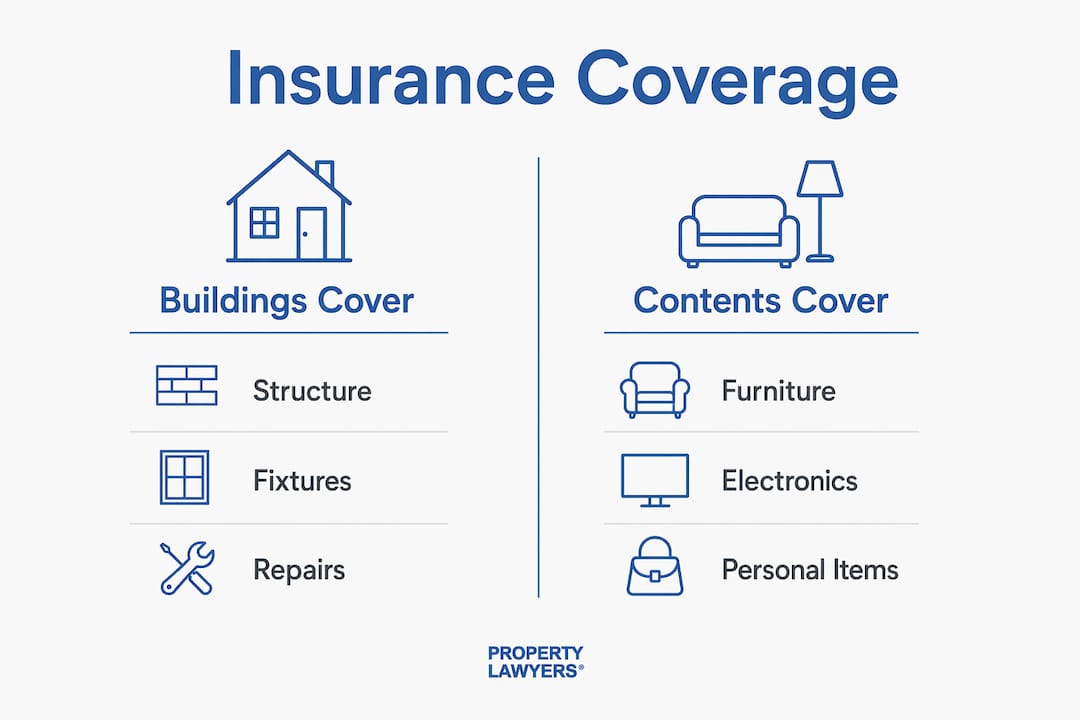

A seguro de hogar bundles three core elements into one policy: buildings cover (continente), contents cover (contenido), and liability insurance (responsabilidad civil). Each element protects a different aspect of your property.

Buildings cover (continente)

Buildings cover protects the physical structure of your property. This includes the walls, roof, floors, fitted kitchens, built-in wardrobes, and permanent fixtures such as plumbing and electrical installations. External features like gates, fences, and swimming pool structures are also typically included. If a fire, burst pipe, or storm damages the fabric of the building, this element of the policy responds.

Contents cover (contenido)

Contents cover protects the movable items inside your home. Furniture, appliances, clothing, electronics, and personal belongings all fall under this category. Policies set a total sum insured for contents, and buyers should check this figure carefully against the actual replacement value of their possessions. High-value items such as jewellery, artwork, and antiques often require separate declarations because standard policies apply sub-limits to valuables. Failing to declare these items can result in a reduced payout or outright claim denial.

Liability and legal protection

Property owner’s liability cover protects you if your property causes injury or damage to a third party. A common example in Spanish apartment buildings is a water leak from your flat damaging the unit below. Without liability cover, you would be personally responsible for the repair costs. Legal protection insurance is commonly included in Spanish home policies and covers legal costs arising from property ownership disputes.

Typical risks covered by a seguro de hogar include:

- Fire and smoke damage

- Water damage from burst pipes or leaks

- Theft and attempted theft

- Storm, wind, and hail damage

- Vandalism

- Natural disasters (via Consorcio de Compensación de Seguros)

Pro Tip: Always read the policy schedule carefully for sub-limits. A policy may advertise €30,000 of contents cover but cap jewellery claims at €1,500 unless you declare items separately.

When is property insurance mandatory in Spain?

Home insurance is not legally required for outright property owners in Spain. However, two situations create a practical or legal obligation to hold cover.

- Mortgage holders. If you finance your purchase with a Spanish mortgage, your lender will require buildings cover for the full duration of the loan. This is standard practice across Spanish banks and is written into mortgage conditions. The lender wants to protect the asset securing the debt.

- Communities of owners. Under the Ley de Propiedad Horizontal, communities of owners must insure shared areas of apartment buildings and urbanisations. This community policy covers communal spaces such as hallways, lifts, and shared pools, but it does not cover the interior of individual flats. Each owner must arrange their own private policy for their unit’s interior.

- Landlords and non-resident owners. While not legally mandated, landlords renting out property in Spain face significant financial exposure without cover. A tenant injury, a fire, or a water leak can generate costs that far exceed a year’s rental income. Non-resident owners should also consider that managing a claim from abroad without insurance support is extremely difficult.

- Holiday rental operators. If you hold a holiday rental licence in Spain, regional authorities in areas like Andalucía and the Balearic Islands may require proof of liability insurance as part of the licence conditions.

- Buyers completing legal due diligence. Insurance requirements often surface during legal checks before purchase, particularly when reviewing community statutes or mortgage conditions.

Pro Tip: Even when insurance is not legally required, the cost of a claim without cover can be devastating. A comprehensive seguro de hogar typically costs a few hundred euros per year. That is a small price relative to the value of a Spanish property.

How does Spanish property insurance work for holiday homes?

Holiday homes and permanent residences are treated differently by Spanish insurers, and the distinction matters considerably for international buyers.

The most important difference involves unoccupancy clauses. For a property declared as a permanent residence, theft cover is typically suspended after 30 consecutive days of vacancy. For a property declared as a holiday home, this limit extends to up to 180 consecutive days. Fire, water damage, and liability cover generally remain active regardless of occupancy status, but theft protection is the element most affected by vacancy.

This means that if you buy a flat in Valencia and declare it as your main home, but then leave it empty for six weeks during summer, your insurer may refuse a theft claim. The solution is straightforward: declare the property as a holiday home from the outset if you do not intend to occupy it year-round.

Declaring property status correctly also affects your premium. Holiday homes typically attract slightly higher premiums than permanent residences because insurers view them as higher risk. An unoccupied property is more vulnerable to undetected leaks, break-ins, and maintenance issues.

| Feature | Permanent residence | Holiday home |

|---|---|---|

| Unoccupancy limit for theft cover | 30 consecutive days | Up to 180 consecutive days |

| Fire and water damage cover | Active regardless of occupancy | Active regardless of occupancy |

| Liability cover | Active regardless of occupancy | Active regardless of occupancy |

| Typical premium level | Standard | Slightly higher |

| Declaration required | Yes, at policy inception | Yes, at policy inception |

Practical steps for maintaining cover on a holiday home:

- Declare the property as a holiday home when taking out the policy

- Arrange for a trusted person to check the property regularly during long absences

- Notify your insurer if the property’s use changes, for example if you begin renting it out

- Review the policy annually to confirm the declared use still matches reality

Common pitfalls when insuring property in Spain

The most costly mistake buyers make is insuring their property at market value rather than rebuild value. These two figures are very different. Market value includes the land, which is not insurable. Rebuild cost, known in Spanish as valor de reconstrucción, covers only the cost of reconstructing the building itself. Insuring at market value leads to over-insurance and unnecessarily high premiums. Insuring below rebuild cost triggers the proportional rule under Spanish law, which reduces any claim payout in proportion to the shortfall. If your property would cost €200,000 to rebuild but you insure it for €100,000, a €50,000 claim may only pay out €25,000.

A second common gap involves the distinction between community insurance and private unit cover. Many buyers in apartment complexes assume the community policy covers everything. It does not. Community insurance covers communal areas only. The interior of your flat, including its fixtures, fittings, and contents, requires a separate private policy. Buyers who skip private cover are exposed to the full cost of any interior damage.

Other frequent mistakes include:

- Failing to declare high-value items such as jewellery, art, or wine collections separately

- Choosing a policy based on headline price without checking sub-limits and exclusions

- Not updating the policy after renovation work that increases the rebuild cost

- Assuming a landlord’s policy covers tenant belongings (it does not)

- Overlooking shared pool liability when purchasing a villa with a communal pool

Insurance brokers consistently stress that policy details matter more than headline prices. A cheap policy with low sub-limits and broad exclusions can leave you significantly underprotected when a claim arises. Working with a qualified broker or a property lawyer who understands the Spanish insurance market helps you identify these gaps before they become expensive problems.

Pro Tip: Ask your insurer or broker for a written breakdown of all sub-limits within the contents section. This single step reveals gaps that the policy summary never mentions.

Key takeaways

Understanding Spanish property insurance correctly from the start protects your investment, satisfies legal obligations, and prevents costly gaps in cover that are difficult to fix after a claim arises.

| Point | Details |

|---|---|

| Seguro de hogar is all-in-one | One annual policy covers buildings, contents, and liability together. |

| Mortgage holders must insure | Spanish lenders require buildings cover for the full life of the loan. |

| Holiday homes need correct declaration | Declare holiday home status upfront to maintain theft cover for up to 180 days of vacancy. |

| Insure at rebuild value, not market price | Using rebuild cost avoids over-insurance and prevents proportional rule penalties on claims. |

| Community cover does not protect your flat interior | Owners in apartment buildings must arrange a separate private policy for their unit. |

My honest view on getting Spanish property insurance right

— Sophie

After years of advising international buyers across Spain, the single issue I see most often is not a lack of insurance. It is the wrong insurance. Buyers arrive with a policy they purchased quickly online, often at the cheapest price available, and they genuinely believe they are covered. Then a water leak damages the flat below, or a break-in occurs during a long absence, and the gaps become painfully clear.

The seguro de hogar system is actually well designed. It is straightforward, affordable, and the inclusion of natural disaster cover via the Consorcio de Compensación de Seguros is a genuine advantage over many Northern European markets. The problem is that buyers do not read the detail. Sub-limits, vacancy clauses, and the distinction between community and private cover are where policies quietly fail people.

My strong advice is to treat insurance as part of your legal due diligence, not as an afterthought. Review your policy every time something changes: after a renovation, after you start renting the property, or after you change your residency status. A property law specialist in Spain can help you understand how your insurance obligations interact with your mortgage conditions, community statutes, and rental licence requirements. That joined-up approach is what protects buyers properly.

— Sophie

How Property-lawyers can help you protect your Spanish investment

Buying property in Spain involves more than finding the right home. Insurance obligations, mortgage conditions, and community regulations all require careful attention before you sign.

Property-lawyers connects international buyers with trusted, independent real estate lawyers across Spain who understand every stage of the purchase process. From reviewing community statutes and mortgage insurance requirements to advising on buying property in Spain with full legal confidence, the lawyers in the Property-lawyers directory are experienced in guiding foreign buyers through the details that matter. If you want qualified legal support from a real estate lawyer in Spain who can review your insurance obligations alongside your purchase, Property-lawyers is the right place to start.

FAQ

Is home insurance legally required in Spain?

Home insurance is not legally required for outright property owners in Spain, but mortgage lenders require buildings cover for the full duration of the loan.

What does seguro de hogar cover?

A seguro de hogar covers the building structure, contents, and third-party liability in one annual policy, with natural disaster cover included via the Consorcio de Compensación de Seguros.

Does community insurance cover my flat interior?

No. Under the Ley de Propiedad Horizontal, community insurance covers shared areas only. Each owner must arrange a separate private policy for their unit’s interior.

How long can my Spanish holiday home be empty before cover is affected?

Theft cover is typically suspended after 30 consecutive days for a permanent residence. For a declared holiday home, this limit extends to up to 180 consecutive days.

Should I insure at market value or rebuild value?

Always insure at rebuild value (valor de reconstrucción). Insuring at market value includes the land, which is not insurable, and insuring below rebuild cost triggers the proportional rule, reducing claim payouts proportionally.

Recommended

- How foreign buyers are protected under Spanish law

- Property law in Spain: a 2026 guide for buyers

- Spanish off-plan property law explained for buyers

- Property Taxes in Spain — Full Guide for Foreign Owners (2026) | Property Lawyers

Sophie Gutenberg is a legal content specialist focused on Spanish property law, real estate transactions, conveyancing, due diligence and tax issues affecting international property buyers in Spain. She works alongside qualified Spanish property lawyers .