Spanish off-plan property law explained for buyers

TL;DR:

- Spanish off-plan property law requires developers to provide individual bank guarantees covering all advance payments for buyer protection. This legal framework ensures funds are held in segregated accounts and grants buyers rescission rights if developers default or delay substantially. Independent legal advice and thorough document verification are essential for international buyers to safeguard their investments in Spain.

Spanish off-plan property law is founded on a legal obligation requiring developers to provide bank guarantees or insurance policies covering 100% of all advance payments made before completion. This framework, established under Law 38/1999 and significantly strengthened by Ley 20/2015, gives international buyers financial protection and enforceable legal rights before a single brick is laid. Understanding these protections is not optional for anyone buying off-plan property in Spain. It is the difference between a secure investment and a costly dispute. This guide covers the core legal provisions, the typical purchase process, the principal risks, and the due diligence steps every buyer must take.

Spanish off-plan property law explained: the legal framework

Spanish off-plan property law governs the purchase of residential property that does not yet exist at the time of sale. The buyer commits funds to a developer based on plans, specifications, and a projected completion date. The law recognises the inherent vulnerability of this arrangement and responds with mandatory protections.

The central protection is the requirement for developers to guarantee all advance payments including VAT and statutory interest at approximately 4% per year, via either a bank guarantee or an insurance policy. This obligation applies from the first payment. Developers must also deposit all buyer funds into a special segregated account, kept entirely separate from their general operating finances. These two requirements together mean that buyer funds cannot be used freely by the developer and must be recoverable if the project fails.

A building licence, known as the Licencia de Obras, must be in place before any legitimate developer requests payment. Contracts must reference a detailed specifications document, define a clear completion date, and include provisions for snagging and warranty periods. These are not optional courtesies. They are legal requirements that form the backbone of a buyer’s protection under Spanish real estate law.

What are the mandatory bank guarantees and how do they protect buyers?

The bank guarantee requirement is the single most powerful protection available to off-plan buyers in Spain. Under Law 38/1999 amended by Ley 20/2015, every advance payment must be individually guaranteed. This means the guarantee covers the exact amount paid, includes VAT and statutory interest, names the buyer, and references the specific unit purchased.

One blanket policy covering an entire development does not satisfy this legal requirement. Individualised guarantee certificates are required for each payment milestone, and each certificate must include the buyer’s name, unit reference, and the precise amount including VAT and interest. This distinction matters enormously in practice. Developers sometimes present a single policy as sufficient. It is not.

Key protections the guarantee framework provides:

- Full deposit recovery if the developer becomes insolvent or fails to deliver

- Statutory interest of approximately 4% per year on all guaranteed amounts

- Legal recourse against the bank if the developer defaults and funds were held in a guaranteed account

- Protection against misuse of funds, since payments must sit in segregated accounts

The consequences of missing guarantees are severe. If a developer accepts payments without providing valid individual certificates, the buyer has grounds to pursue the bank directly. Spanish Supreme Court rulings have confirmed that banks are jointly liable for refunding deposits if they allowed payments into accounts without valid guarantees in place. This is a significant legal safety net, but it only applies when buyers have documented their payments correctly.

Pro Tip: Request a fresh, individualised guarantee certificate before making every milestone payment. Do not accept verbal assurances or a reference to an existing blanket policy. Your independent lawyer should verify each certificate before funds are transferred.

How does the off-plan purchase process in Spain work?

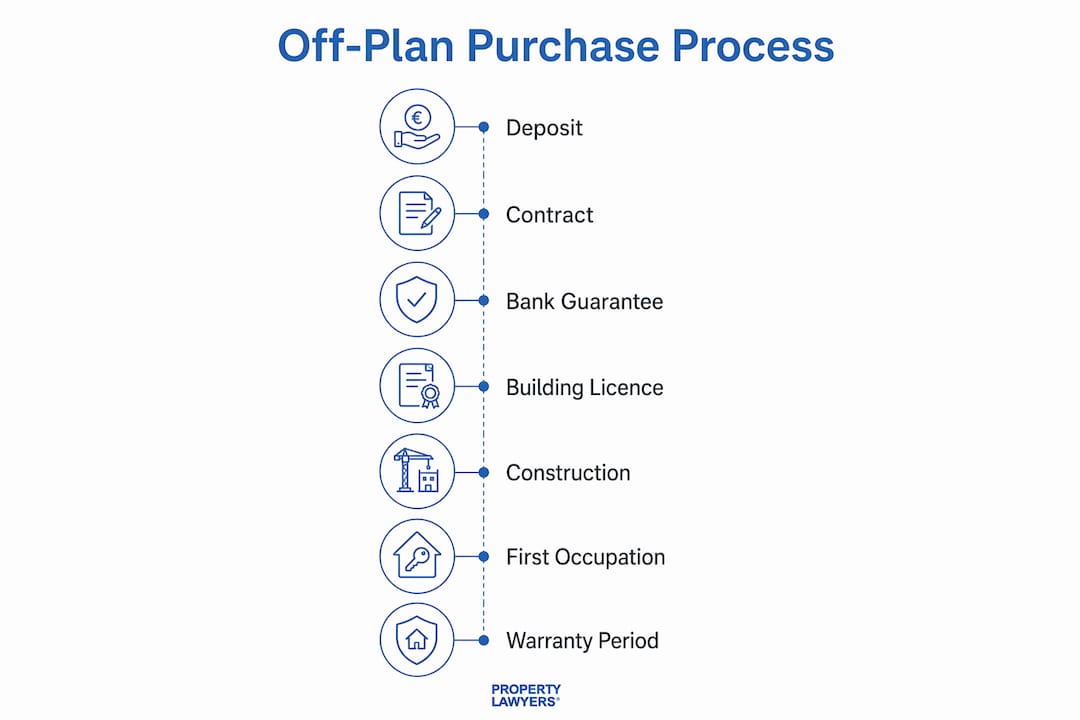

The typical off-plan transaction in Spain follows a structured sequence of stages, each with distinct legal and financial implications. Understanding this sequence is fundamental to buying property in Spain without unnecessary exposure.

- Reservation deposit: Typically between €3,000 and €10,000, paid to secure the unit and remove it from the market. This is usually non-refundable if the buyer withdraws without legal cause.

- Private purchase contract: Signed within weeks of the reservation, this is the binding agreement. It requires a payment of 20% to 30% of the purchase price and must include the full specifications document, completion date, penalty clauses, and guarantee details.

- Stage payments during construction: Milestone payments tied to construction progress, each requiring a new individualised guarantee certificate.

- Pre-completion snagging: The buyer inspects the finished property, documents defects, and agrees a snagging list with the developer before signing the final deed.

- Final deed and balance: The escritura is signed before a notary, the final balance is paid, and title transfers to the buyer.

“Contracts should explicitly define valid delays and penalties. Vague completion dates such as ‘Q3 2027’ are insufficient and legally risky for buyers. Specifics reduce disputes and strengthen buyer protections.” — Off Plan Property Spain Guide

Warranty periods under Spanish law are structured in three tiers: one year for finishing defects, three years for habitability defects, and ten years for structural defects. These periods run from the date of the escritura, not from when you first notice a problem. Buyers should record all defects formally and in writing from the moment they take possession.

The License of First Occupation, known as the Licencia de Primera Ocupación, is a non-negotiable prerequisite before signing the final deed. Without it, the property cannot legally be occupied, and utility connections cannot be established. Signing the escritura before this licence is granted creates serious practical and legal problems.

What are the common risks and legal remedies if the developer fails?

Off-plan property investment in Spain carries real risks. Developer insolvency, project abandonment, and significant construction delays are not theoretical concerns. They have affected thousands of buyers, particularly during the 2008 financial crisis and in subsequent downturns. Understanding the legal remedies available is as important as understanding the protections.

The principal risks buyers face include:

- Developer insolvency before project completion, leaving buyers without a property and potentially without their deposits

- Project abandonment where construction halts indefinitely without formal insolvency proceedings

- Substantial delays beyond the contracted completion date, disrupting financing, relocation plans, and rental income projections

- Specification changes where the finished property differs materially from what was agreed in the contract

If a developer fails to deliver on time, buyers have the legal right to rescind the contract and demand a full refund plus interest, either from the developer directly or from the bank holding the guaranteed deposits. This right is enforceable when the delay is substantial and unjustified. The contract must define what constitutes a valid delay and what triggers the buyer’s right to exit.

Spanish Supreme Court rulings have gone further, holding financial institutions jointly liable when they accepted deposits into accounts without valid guarantees. Buyers have successfully claimed refunds from banks years after the original transaction, even when the developer no longer existed. This precedent is powerful, but it requires buyers to have maintained proper documentation throughout.

Pro Tip: Keep copies of every payment receipt, every bank transfer confirmation, and every guarantee certificate in a secure location. If a dispute arises years later, this documentation is what makes a claim viable.

How to verify legal documents and licences before committing

Due diligence on an off-plan purchase in Spain is not a formality. It is the process by which you confirm that the developer has legal authority to build, that your funds will be protected, and that the project is financially and legally viable. Independent legal checks before any payment is made are the most effective way to avoid costly mistakes.

The key checks to complete before committing to any off-plan purchase:

- Licencia de Obras: Confirm the building licence has been granted by the local authority before making any payment. A developer requesting funds before this licence exists is operating outside the law.

- Mercantil registry: Verify the developer’s company registration, financial standing, and any existing embargoes or creditor claims against the business.

- Segregated bank account: Confirm that a special account exists for buyer payments and that it is separate from the developer’s operating accounts.

- Guarantee certificates: Have your lawyer verify that individual guarantee certificates are in place for each payment before funds are transferred.

- License of First Occupation: Confirm this will be obtained before the final deed is signed. Never complete without it.

| Check | Who verifies it | When to complete |

|---|---|---|

| Licencia de Obras | Independent lawyer | Before reservation payment |

| Developer registration | Independent lawyer | Before private purchase contract |

| Segregated account | Independent lawyer | Before any payment |

| Guarantee certificates | Independent lawyer | Before each milestone payment |

| License of First Occupation | Independent lawyer | Before final deed signing |

Independent legal counsel is critical because a developer’s appointed lawyer represents the developer’s interests, not yours. The developer may recommend a lawyer or notary. You should appoint your own. The cost of independent legal advice is a fraction of the financial exposure you carry without it.

What practical considerations must international buyers mind?

International buyers face additional layers of complexity when purchasing off-plan property in Spain. Beyond the legal framework, there are financial and logistical factors that can materially affect the outcome of the investment.

Payment timing and currency risk are two of the most underestimated challenges:

- Currency exposure: A 5% adverse currency movement on a €280,000 purchase over an 18-month construction period can cost €14,000 in unexpected additional cost. Forward contracts with a currency specialist lock in an exchange rate and eliminate this uncertainty.

- Construction delays: Delays of six months or more are common in Spanish off-plan projects. Build a timing buffer into any relocation or rental income plan. Do not commit to a lease end date that assumes on-time delivery.

- Mortgage timing: Spanish mortgage offers typically have a validity period of three to six months. If completion is delayed, you may need to reapply, potentially at a different rate.

- Snagging retention: Retain a small percentage of the final payment until the agreed snagging list is resolved. This is not always standard practice in Spain, but it is a legitimate negotiating point.

Pro Tip: Engage a currency specialist before signing the private purchase contract, not at the point of final payment. Locking in a rate early removes one significant variable from an already complex transaction.

The Spain property investment guide for 2026 reflects a market where demand from international buyers remains strong, particularly on the Costa del Sol, in Valencia, and in the Balearic Islands. That demand does not reduce the legal risks. It makes thorough preparation more important, not less.

Key takeaways

Spanish off-plan property law requires developers to provide individualised bank guarantees for every advance payment, and buyers who verify these protections before each transaction stage have the strongest legal position if a developer fails.

| Point | Details |

|---|---|

| Bank guarantees are mandatory | Every advance payment must be covered by an individualised certificate naming the buyer and unit. |

| Segregated accounts protect funds | Developer payments must be held separately from operating finances and cannot be freely used. |

| Rescission rights are enforceable | Buyers can recover all payments plus interest if a developer delays substantially or becomes insolvent. |

| Banks carry joint liability | Spanish Supreme Court rulings confirm banks are liable if they accepted deposits without valid guarantees. |

| Independent legal advice is non-negotiable | A developer’s lawyer acts for the developer; buyers must appoint their own counsel for every stage. |

Why independent legal advice is the only real protection you have

After working with international buyers on Spanish property transactions for many years, the pattern I see most often is this: buyers who encounter problems almost always skipped independent legal advice at one or more stages. They relied on the developer’s recommended lawyer, accepted a blanket guarantee policy without question, or signed a contract with a vague completion date because the sales agent assured them it was standard.

The law in Spain is genuinely protective of off-plan buyers. The bank guarantee framework, the segregated account requirement, and the Supreme Court rulings on bank liability together create a strong safety net. But that safety net only catches you if you have followed the correct procedures at every stage. A guarantee certificate that does not name you individually is worthless. A contract that defines completion as “approximately Q3 2027” gives you almost no legal leverage if the developer delivers in Q1 2028.

The buyers I have seen recover their deposits after developer insolvency had one thing in common: meticulous documentation and an independent lawyer who verified every certificate before every payment. The buyers who lost money had the opposite. They trusted the process without verifying it.

Off-plan property in Spain remains one of the more attractive investment propositions in Europe, particularly in coastal and urban markets where new supply is constrained. The legal framework is sound. The risks are manageable. But they require active management, not passive trust in the developer’s assurances.

— Sophie

How Property-lawyers can protect your off-plan investment

Purchasing off-plan property in Spain without specialist legal support exposes you to risks that are entirely avoidable. Property-lawyers connects international buyers with trusted, independent real estate lawyers in Spain who specialise in off-plan transactions and understand every stage of the legal process.

The lawyers in the Property-lawyers network provide independent contract reviews, verify building licences and developer credentials, confirm that guarantee certificates are legally compliant before each payment, and represent buyer interests if a developer fails to deliver. Whether you are purchasing on the Costa del Sol, in Madrid, or in the Balearic Islands, find a specialist lawyer through Property-lawyers before you commit to any payment. The right legal advice at the right time is the most cost-effective investment you will make in the entire transaction.

FAQ

What does Spanish off-plan property law require from developers?

Spanish law requires developers to provide individualised bank guarantees or insurance policies covering 100% of all advance payments, including VAT and statutory interest at approximately 4% per year. All buyer funds must be held in a special segregated account separate from the developer’s general finances.

Can I get my deposit back if the developer goes bankrupt?

Yes. If the developer becomes insolvent or fails to deliver the property, buyers have the legal right to rescind the contract and recover all payments plus interest, either from the developer or from the bank holding the guaranteed deposits. Spanish Supreme Court rulings confirm that banks are jointly liable if they accepted deposits without valid guarantees.

What is the License of First Occupation and why does it matter?

The Licencia de Primera Ocupación is a licence issued by the local authority confirming that the completed property meets habitability standards and building regulations. It is required before utility connections can be established and before the final deed should be signed. Completing without it creates serious legal and practical complications.

How much should I expect to pay at each stage of an off-plan purchase?

Reservation deposits typically range between €3,000 and €10,000. The private purchase contract requires a further payment of 20% to 30% of the purchase price. Stage payments follow during construction, with the final balance paid at completion when the escritura is signed before a notary.

Why should I appoint an independent lawyer rather than use the developer’s recommended one?

A developer’s appointed lawyer acts exclusively in the developer’s interests. An independent lawyer verifies building licences, reviews guarantee certificates, checks the developer’s registration and financial standing, and ensures the contract protects your rights. This distinction is the most important decision you will make in the entire purchase process.

Recommended

- Spanish real estate law: a buyer’s guide for 2026

- Spanish property contracts explained: a buyer’s guide

- Property law in Spain: a 2026 guide for buyers

- How Spanish wills protect property buyers

Sophie Gutenberg is a legal content specialist focused on Spanish property law, real estate transactions, conveyancing, due diligence and tax issues affecting international property buyers in Spain. She works alongside qualified Spanish property lawyers .